The Definitive Guide to Usage-based Car Insurance

Free Auto Insurance Comparison

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Brad Larson

Licensed Insurance Agent

Brad Larson has been in the insurance industry for over 16 years. He specializes in helping clients navigate the claims process, with a particular emphasis on coverage analysis. He received his bachelor’s degree from the University of Utah in Political Science. He also holds an Associate in Claims (AIC) and Associate in General Insurance (AINS) designations, as well as a Utah Property and Casual...

Licensed Insurance Agent

UPDATED: Nov 28, 2023

It’s all about you. We want to help you make the right legal decisions.

We strive to help you make confident insurance and legal decisions. Finding trusted and reliable insurance quotes should be easy. This doesn’t influence our content. Our opinions are our own.

Editorial Guidelines: We are a free online resource for anyone interested in learning more about insurance. Our goal is to be an objective, third-party resource for everything legal and insurance related. We update our site regularly, and all content is reviewed by experts.

UPDATED: Nov 28, 2023

It’s all about you. We want to help you make the right legal decisions.

We strive to help you make confident insurance and legal decisions. Finding trusted and reliable insurance quotes should be easy. This doesn’t influence our content. Our opinions are our own.

On This Page

Introduction

“The one thing that unites all human beings, regardless of age, gender, religion, economic status or ethnic background, is that, deep down inside, we ALL believe that we are above average drivers.”

– Dave Barry

Usage-based insurance (UBI) can help you save a fistful of dollars on car insurance. The basic principle behind UBI is outlined in its name, you pay only for what you use. By proving that you’re a good driver or don’t put a lot of miles on your car, insurers will lower your premiums – sometimes up to 50%. You can’t get that kind of discount using traditional car insurance plans, no matter how many defensive driving courses you take.

While UBI may help you save a bundle of cash, you still need to consider a few things about this relatively new form of car insurance. Its savings come from letting insurers track how, when, and sometimes, where you drive. That can leave a lot of people feeling like they just stepped into Orwell’s 1984. Also, if you sign up for the wrong type of UBI, you may actually end up paying more for car insurance than you were before.

Here’s what UBI can potentially do for you:

- Get personalized rates that may be way lower than what you’re paying now

- Receive instant feedback on your driving habits, helping you drive better when you’re behind the wheel

- Track your car down if it’s stolen

Use this guide to easily find out how to take advantage of these lower premiums with UBI, or sleep easier at night knowing your traditional car insurance was the best deal all along.

Table of Contents

Chapter 1: How the individualized prices of usage-based car insurance can slash your premiums

Chapter 2: Know the difference between pay-as-you-drive and pay-how-you-drive to get more mileage out of your savings

Chapter 3: Car talk- Choosing the right way for your car to transmit driving data to your insurer

Chapter 4: Protect your privacy by discovering what UBI plans can do with your data

Chapter 5: The best ways for accelerating your UBI premium discounts

Chapter 6: Avoid paying more with UBI by putting the brakes on these driving habits

Chapter 7: Six different UBI plans on the market, six different ways to save

Chapter 8: This easy quiz will help tell you if UBI is right for you

Chapter 1

How the individualized prices of usage-based car insurance can slash your premiums

Insurers worked on UBI for years before they started selling it, with Progressive patenting a device for determining personalized car insurance rates way back in 1996. That’s a lot of time spent mulling over how they – and you – can save money. Here’s how it works, and what’s different about it than the plans most people have now.

How traditional car insurance works

Traditional car insurance plans base their premiums on past data. Insurance companies look at a customer’s age, whether they drive a luxury roadster or a clunker, if they frequently get into accidents and a huge number of other factors. Using this information, the insurer calculates a rate based on how often people with similar characteristics got into wrecks or filed a claim for other reasons.

You may be paying too much for car insurance

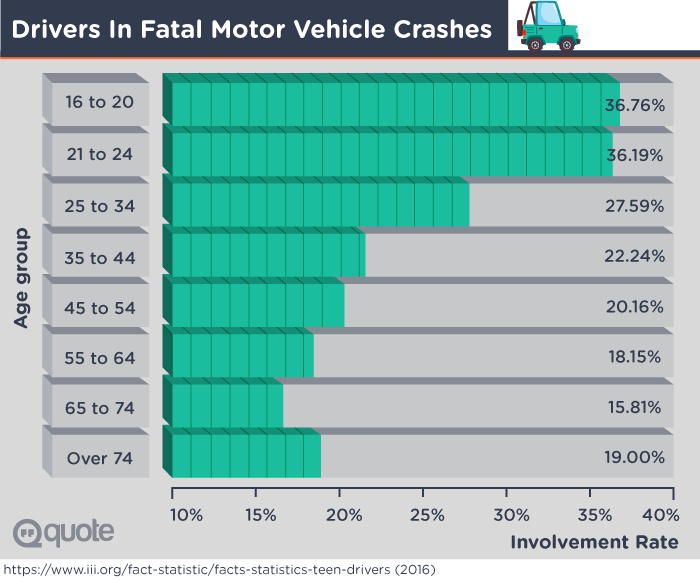

Basically, this pricing method relies on estimates of how people probably drive, rather than how they actually behave on the road. For example, even if an 18-year-old driver is a good driver with the self-control of a saint, traditional car insurance plans will still charge them a higher rate because teenagers statistically get into more accidents – three times more than drivers over the age of 20, according to the Insurance Institute for Highway Safety.

How UBI calculates more accurate rates

In contrast, UBI prices rely on your individual driving habits. As the National Association of Insurance Commissioners explains, “UBI programs seek to convert the fixed costs associated with mileage driven into variable costs that can be used in conjunction with other rating factors in the premium calculation. UBI has the advantage of utilizing individual and current driving behaviors, rather than relying on aggregated statistics and driving records that are based on past trends and events, making premium pricing more individualized and precise.”

Instead of assuming that everyone in a certain demographic is at the same risk of getting in an accident, UBI lets insurers calculate rates based on the way individual people drive. Returning to that previously mentioned fictional 18-year-old driver, enrolling in UBI would let the car insurance company see that he doesn’t treat driving like an audition for The Fast and the Furious. Because of that knowledge, the insurer would cut the teenager a lower rate for his good driving habits.

You need to opt-in to save

Since safe or infrequent drivers get in fewer wrecks, insurers spend less money on paying out their claims. UBI lets you prove you’re one of these low-risk drivers and slashes your premiums as a result. None of the UBI plans currently on the market are mandatory or auto-enroll drivers, so you’ll need to sign up to see if you qualify for a discounted rate.

The different UBI programs on the market will be coming up in chapter 7, but for right now it’s time to talk about the two main types of these price-lowering plans.

Chapter 2

Know the difference between pay-as-you-drive and pay-how-you-drive to get more mileage out of your savings

Two types of UBI: Pay-as-you-drive and pay-how-you-drive. Which one are you?

UBI plans typically fall into the categories of either pay-as-you-drive or pay-how-you-drive car insurance, both of which target specific kinds of drivers. You may only get on the road once in a blue moon, but drive like you’re drag racing every time. You might put hundreds of miles on your car per month without even the slightest of fender benders. You probably fall somewhere between these extremes (hopefully). No matter how you drive, signing up for the wrong plan will hit your pocketbook. Here’s how you figure out which type you are.

You can also see chapter 8 for an easy quiz to determine which type is best for you.

TYPE 1

Pay-as-you-drive insurance (PAYD) is meant for people who clock few miles driving

A car in a garage gets in fewer accidents than a car on the road. That’s the underlying philosophy behind pay-as-you-drive (PAYD) car insurance, also known as pay-per-mile insurance. Metromile, an insurer offering this type of UBI, explains the pricing scheme like this:

“With pay-per-mile insurance you pay a low monthly base rate plus a few cents per mile when you drive. At the end of the month, your bill is your base rate plus how many miles you drove at your per-mile rate. Just like with other insurance companies, several factors can influence your rate, including age, type of vehicle, and driver history.”

This plan is perfect for people who work from home, have a short commute, or don’t drive that often but like to absolutely floor it (with safety and responsibility in mind) when they do.

TYPE 2

Pay-how-you-drive insurance (PHYD) is meant for careful drivers

Mileage rates also factor into PHYD car insurance. Like the name says, this program looks at how people drive to determine their premiums. PHYD tracks driving data including:

- When you drive: Is it at night, when the risk of a fatal crash is three times higher, or during safer daylight hours?

- Where you drive: Are you putting a lot of miles on your car, or spend a lot of time driving during accident-inducing rush hour traffic?

- How fast you brake or accelerate: If you’re regularly slamming on either pedal as soon as the light turns green or red, that’s just plain dangerous.

Going back to the National Association of Insurance Commissioner report, after collecting this data, an insurance company then “assesses the data and charges insurance premiums accordingly. For example, a driver who drives long distance at high speed will be charged a higher rate than a driver who drives short distances at slower speeds.”

Don’t choose a plan just yet

Before picking a plan based on how much or safe you drive, there’s a whole host of other factors to consider. You need to think about what data you’re comfortable sharing with insurers – and how they collect it.

Chapter 3

Car talk- Choosing the right way for your car to transmit driving data with your insurer

Data collection: A must for UBI

Without data on your driving, UBI plans can’t accurately calculate your hopefully-reduced rates. Different plans use different methods for collecting this information. By understanding the various ways insurers monitor your driving habits, you can decide which methods you’re comfortable with and which you’d rather avoid. No matter what data-tracking choice you make, it will be a form of what’s called telematics.

What are telematics?

In a nutshell, telematics are the different methods for transmitting data from your car to your insurer. That makes them the engine powering all UBI programs, as this data is necessary for a car insurance company to calculate your personalized rate. Both PHYD and PAYD plans use these devices for monitoring how safe and how often people drive. Most drivers will be familiar with at least one of the three forms of telematics insurers use to collect information.

- OnStar and SYNC: Anyone who’s called for a tow using OnStar or sent a text using SYNC is already familiar with telematics. Insurance programs like the State Farm Drive Safe and Save plan use these built-into-you-car communication platforms to monitor mileage and other driving habits – after all, that’s what the device is meant to do.

- Plug-In Devices: For PHYD customers without OnStar or Sync, many insurers usually offer a small telematics device that can be used in cars built after 1996. For these newer cars, the device plugs into a vehicle’s on-board diagnostic port (though it needs to be an OBD-II port, as the ports for older cars are not compatible with these devices). That’s the same port mechanics use to get the error code for whatever causes your check engine light to start glowing. UBI plans don’t track whether your radiator is low on coolant, though, as connecting the telematics device into the OBD-II port only allows it to gather data from your car about when, how, and sometimes, where you drive. This information is then sent straight to your insurer. This lets your car insurance company either track just mileage driven in the case of PAYD plans like MetroMile, or g-forces and sudden changes in speed for participants in Progressive’s Snapshot program.

- Smartphone App: Unfortunately some cars built before 1996 have an incompatible onboard diagnostic port for telematics devices. An article in Wired mentions how some insurers have begun offering a “smartphone app to consumers, who use the technology in their cars in exchange for a possible discount.” That means if you’re the proud owner of a classic ’55 T-Bird without one of these ports, you can still add your roadster to a UBI plan offering smartphone telematics. See a list of some popular UBI plans in chapter 6.

So what’s the cost of a plug-in device?

Right now there’s no charge for any of these devices. It’s similar to Google, where you can use it for free in exchange for letting the company peek at some of your data. The plug-ins are also easy enough to install that you can do it yourself. Just don’t lose one, or that could run you $100 if you’re a Metromile customer.

When it comes to telematics, focus on what data they collect

So phones, plug-ins and cars themselves can tell insurers whether you’re a good driver or a speed demon by monitoring when, how, and where you drive every time you get behind the wheel. The important thing about choosing a telematics device is making sure it’s compatible with your car. The real big question you need to chew on is how much driving data you’re comfortable sharing with your insurer through this device.

Chapter 4

Protect your privacy by discovering what UBI plans can do with your data

Should I worry about my car insurance company tracking my driving data?

According to a 2016 Pew Research Center Poll, almost half of Americans find the thought of any company knowing where and how they drive downright creepy:

“Some 45% say they would find the following tradeoff of personal information for benefits to be not acceptable:

“Your insurance company is offering a discount to you if you agree to place a device in your car that allows monitoring of your driving speed and location. After the company collects data about your driving habits, it may offer you further discounts to reward you for safe driving.”

The thought of the details of every trip ending up in a database can make folks nervous. However, there are limits to how much personal information UBI providers can collect, and what they can and can’t do with it. You can use this knowledge to pick a plan that’s right for your expected level of privacy – or even uses your data to help find your stolen car, or get out of a sticky situation with the law.

Your plan can only collect so much data

Every plan places limits on what data it collects, and how it is used. The amount of data collected on a driver will vary based on which program they select. For instance, Esurance’s pay-per-mile program monitors only a car’s mileage and GPS location, while SmartRide from Nationwide detects the number of miles driven, as well as accident-causing factors like hard braking and acceleration, idle time, and nighttime driving.

UBI programs don’t sell data to third parties – yet

UBI programs don’t currently sell driver information to third-parties. That means you won’t receive Twitter ads for Taco Bell just because you’ve gone through their drive-thru 15 times in the past week, or see higher health insurance prices if your erratic driving increases the risk of a nasty car wreck.

That doesn’t mean this won’t change in the future. In 2015, a Bloomberg article quoted Allstate’s CEO as saying, “Could we, should we sell this information we get from people driving around to various people and capture some additional profit source and perhaps give a better value proposition to our customers?” Insurers might offer data for sale just like Facebook or Google in the coming years, but so far this hasn’t happened yet.

What insurers CAN do with your data

For the most part, insurers exclusively use this data for adjusting the price of premiums. There are a few instances when UBI plans can share personal data with outside parties:

Monitor fraud

A study by the Center for Insurance Policy and Research describes how companies can spot fraudsters using data. “By combining driving information with mapping technology, insurers have additional evidence to consider when investigating claims. If, when and where an incident occurred may be corroborated or disputed by data received through the use of telematics.”

This goes far beyond detecting when someone reports they were in a non-existent collision hoping for a payday. Insurance prices vary from ZIP code to ZIP code. GPS data can rat out people who live in an expensive area but register their car in a cheaper one. Also, car insurance companies require drivers for Uber and Lyft to take out business or specific rideshare policies on their cars. If a telematics device notices a person driving back and forth from the airport three times a day on a personal auto insurance policy, their insurer could notice they’re working for a rideshare app and drop them.

Find your stolen car

Sometimes knowing where your vehicle is at all times can come in handy. If someone finds their set of wheels stolen, their car can be easily tracked down if it’s equipped with a location-monitoring device.

Report on (or defend against) criminal actions

While your car won’t snitch about being double parked, Progressive’s Snapshot program states it will share information “when we’re legally required to provide the data, such as in response to a subpoena in a civil lawsuit or by police when investigating the cause of an accident.” That means bank robbers using their telematics-equipped vehicle as a getaway car will have much bigger worries than pricier auto insurance.

On the flipside, it can get drivers out of wrongfully issued speeding tickets, as one London man discovered. He was fined £100 for speeding in London – but the telematics in his car proved he had been in a completely different city at the time of the citation.

What if I cancel my UBI plan?

Canceling PAYD plans means switching insurance completely. All the current PHYD programs are currently optional though, so opting out of them won’t affect your rates. In the case of Progressive, you may incur a surcharge when you renew your policy if you cancel after 45 days from when you signed up. Meanwhile, your data stays with the insurer after you’re done with the plan. It’s still protected though, kept under the digital equivalent of lock and key to make it as far out of reach from hackers as possible.

So should I be scared about sharing my data or not?

According to the consulting firm Deloitte, any privacy concerns about UBI should be considered in context of “the multitude of other technologies already in play to monitor driving, including “black boxes” installed by the manufacturer, the proliferation of traffic cameras, and even the data collected by their own smartphones just by being turned on, beyond any telematics insurance application.”

Since all this data tracking makes people nervous, UBI insurers are being very careful with data right now. Metromile allows you to turn off the location tracking feature on its plug-in device, while Allstate promises that “no location services information is available to the people servicing a policy.” Basically you can choose what you share with your insurer, and they’ll make sure your insurance agent doesn’t keep tabs on your comings and goings.

Chapter 5

The best ways for accelerating your UBI premium discounts

How to get and keep discounted rates with UBI

If you’ve decided letting insurers track your driving capabilities is worth lowering your monthly premiums, it’s time to plan how you can maximize your potential discount – which clocks in at around 10% on average. Some of these plans even offer ways of making you drive safer, helping you cut even more off your premiums than the average saver. If you don’t learn about all the different factors that can affect your insurance costs, you risk getting a negligible reduction – or worse, even increased rates, if you drive poorly.

How much can I expect to save?

Different insurers offer different savings when it comes to UBI. Drive Safe and Save plan promises discounts up to 50% for good drivers, while Nationwide’s SmartRide program advertises a potential 40% rate reduction.

Most drivers won’t receive the maximum deduction of course, but The Saunders School of Business conducted a 2016 study on a large insurer offering UBI and found that “the average discount rate is 12% with a standard deviation of 5%” for most drivers. That’s a hefty chunk of change saved each year just by using these plans.

Your device wants to help you drive

PHYD forms of UBI let folks turn safe driving into saved money. Luckily, some telematics can help people drive better in real time. For example, Progressive’s Snapshot plug-in device starts beeping when drivers make a hard brake, reminding them that this behavior is dangerous. That lets you instantly know when you’re in danger of losing your lower premiums – and in danger of an accident.

Of course, some people find any device that beeps whenever they might be losing money annoying. As Joe Manna states in his awesomely comprehensive review of Progressive’s Snapshot:

“Ask any Snapshot driver about what they don’t like about the program. When they hear the “BEEP-BEEP-BEEP” produced from the device, they know exactly what happened. It means they just got ratted out to Progressive for slowing down just a little too fast.”

When will my discount take effect?

Some programs also offer lower premiums just for signing up. People who enroll in the Nationwide’s SmartRide program instantly get 10% off their rates just for joining. PHYD plans usually apply all discounts at when your lease is renewed, typically after six months. This pricing scheme doesn’t apply to PAYD members, as they only pay for the miles they drive.

Drive safe, save more

Good drivers who save money on UBI follow these safety-minded habits:

- Avoid night driving: Nothing good ever happens after midnight – especially for insurance rates. Drunk and drowsy drivers are most frequently on the road between the witching hour and 4 a.m., so insurers decrease rates for people who don’t spend a lot of time behind the wheel during this timeframe.

- Stay away from rush hour: Accidents are also more likely to occur during rush hour. You can reduce both your premiums and stress by avoiding peak commuting hours.

- Drive less: This tip is most important for PAYD plans. After all, a car in a garage is worth ten in a pile-up. Driving fewer miles will result in a fatter wallet.

- Keep the needle under 80: Few things feel better than hearing a powerful engine roaring down the highway. According to car insurance companies, one of those few things is saving money by maintaining a safe speed below 80 miles per hour.

- Avoid hard acceleration and braking: Insurers will cut their rates for drivers who don’t put either pedal to the metal. Save big by avoiding accelerating more than 5 miles per hour in one second, or braking more than 7.7 miles per second.

- Don’t be idle: After all, idle cars are the devil’s playground. More accidents happen in stop and go traffic, so keep moving by keeping away from congested streets.

Take fewer risks, save more dollars

Keeping in mind what insurers track when you’re on the road helps you maintain a healthy discount. The key thing to remember is that when you drive safe and drive less, you save money.

Chapter 6

Avoid paying more with UBI by putting the brakes on these driving habits

The good news is that some UBI plans like SmartDrive from Nationwide won’t increase rates even for drivers who spend all night hurtling down the road at teeth-rattling speeds. The bad news is that some programs do. Basically, there are two different ways you can avoid raising your premiums with UBI: drive responsibly and smartly (see chapter 5 for tips on specific things you can do to lower your UBI rates and/or prove your a responsible and safe driver) and keep your mileage low.

Poor driving increases UBI prices for some plans

Progressive’s Snapshot program falls into the latter category, stating that while most drivers earn a discount, riskier drivers whose habits “indicate a greater likelihood of being in an accident and may result in a higher rate at renewal.”

Some of the factors PHYD plans monitor may be unavoidable for certain drivers. People who spend a lot of time in rush hour or work night shifts could see their premiums increase.

Insurers are serious about making you pay per mile

Drivers with a long commute could also see rates go up using both PHYD and PAYD programs. Esurance Pay Per Mile states that drivers who don’t tack on 10,000 miles to their odometers per year can see lower car insurance premiums. The average American drives 13,476 miles per year according to the Federal Highway Administration, so most folks would do well to check that their annual mileage is well below average before signing up.

Putting heavy miles on a car can also cause the removal of pre-existing discounts under UBI plans. Drive Safe and Save plan states it only collects information to apply a discount. That is, unless they discover “you currently receive a premium reduction for low estimated annual mileage (under 7,500 miles annually for personal use) and your vehicle is actually driven more than that, your premium may increase at a future policy renewal period.” Translation? Avoid driving more miles than you said you would to keep your premiums from changing.

By knowing your mileage and carefully considering how you drive, you can avoid the typical reasons UBI providers raise your rates. Choose the plan that fits your driving style, or seek out other insurance alternatives.

Chapter 7

Six different UBI plans on the market, six different ways to save

Find out what programs are out there

Drivers considering enrolling in a UBI program have a variety of choices. Here’s a selection of some of the different plans on the market:

- Type of insurance: PAYD program

- Telematics: Plug-in device

- Data tracked: Mileage only

- Available discounts: Calculates a base rate like traditional insurance, then charges a few cents for each mile driven

- Discount applied: N/A

- Possibility for higher rates: Yes, if driver exceeds 10,000 miles on insured vehicle per year

- Type of insurance: PHYD

- Telematics: Plug-in device

- Data tracked: Mileage, the amount of time spent driving, time of day spent driving, hard braking, rapid acceleration, vehicle identification number. Snapshot also tracks location data for research and development purposes, but this is not used to calculate rates

- Available discounts: 10% participation discount upon enrollment, maximum discount of 20% – 30% dependent on state applied at policy renewal

- Possibility for higher rates: Yes, up to 10%

- Type of insurance: PHYD

- Telematics: Smartphone app or plug-in device

- Data tracked: Mileage, hard braking and acceleration, idle time, nighttime driving

- Available discounts: 10% participation discount applied immediately, 40% maximum discount applied after 4-6 months

- Possibility for higher rates: No

- Type of insurance: PHYD

- Telematics: Plug-in device

- Data tracked: Time of day and amount of time spent driving, mileage, hard braking and acceleration

- Available discount: 5% participation discount applied immediately, average final discount estimated between 10%-12% during the policy renewal

- Possibility for higher rates: No

- Other restrictions: The Hartford offers insurance exclusively for AARP members. Diesel, hybrid and electric cars are also ineligible for TrueLane

Drive Safe and Save and Drive Safe and Save Mobile from State Farm:

- Type of insurance: PHYD

- Telematics: OnStar and SYNC platforms for Drive Safe and Save, or smartphone app for Drive Safe and Save Mobile

- Data tracked: Mileage, basic driving characteristics

- Available discounts: 5% participation discount applied immediately, up to 50% discount upon policy renewal

- Possibility for higher rates: Not based on driving data, but can remove existing premium reduction for low estimated annual mileage if the insured vehicle is driven over 7,500 miles per year

Chapter 8

This easy quiz will help tell you UBI is right for you

If you’re curious whether UBI could start saving you money for being an infrequent or good driver, you should ask yourself a few simple questions. Answer these and learn which program type of UBI (if at all) is good for you.

1. How much do you drive?

- A. Under 10,000 miles

- B. Over 10,000 miles

- C. I live my life on the road and off the grid.

2. Have you had any accidents, traffic tickets, or other rate-raising incidents over the past year?

- A. Yes

- B. No

- C. Traffic tickets? According to the government, I don’t even exist!

3. Do you do most of your driving late at night or during rush hour?

- A. Yes

- B. No

- C. Why are you asking so many questions, is this an interrogation?

4. How much data are you comfortable sharing with your insurer?

- A. Somewhat comfortable

- B. Very comfortable

- C. No way, I even protect my thought data with a tinfoil hat.

5. Would you like to be able to track your car’s location in case of theft?

- A. That doesn’t matter to me

- B. Yes

- C. Are you kidding? I don’t even let me track myself – Wait, where am I?

If you answered A to most of the questions above, you’ll likely want to go with a PAYD insurer like Metromile.

If you answered mostly Cs, you need advice that’s far outside the scope of this guide.

For those of you with a majority of B answers, you’re probably looking at PHYD insurance.

Time to keep narrowing down your options:

1. I’m an AARP member who doesn’t drive an electric, diesel or hybrid car

- Yes

- No

2. I’d like immediate feedback when I’m driving in ways that may lower my premium discount

- Yes

- No

3. I would prefer to use my phone rather than a plug-in device for data collection, or I will be insuring a car made before 1996

- Yes

- No

4. I would like to use the OnStar or LYNC system already included with my car to transmit data to my insurer

- Yes

- No

If you answered yes to the first question, you should consider TrueLane from The Hartford.

For the second question, answering yes means you may be a perfect candidate for Snapshot from Progressive.

As those answering affirmative to the third question, think about using either Drive Safe and Save Mobile or SmartDrive from Nationwide.

In the case of a yes to the fourth question, that means you may prefer State Farm’s regular Drive Safe and Save program.

Now you can decide if UBI is right for you

By now you should be feeling like an expert on how UBI works. Take it or leave it, at least, you are well informed. You know that to get potential discounts and avoid rate-rising pitfalls you’ll have to think carefully about your driving needs, data privacy, and how committed you are to driving responsibly. Saving money – as much as 40% each month!!! – on car insurance can be the difference between taking a vacation or not each year , which is why it’s important to know your stuff and shop around. With this definitive guide to usage-based car insurance, you are well prepared to reach out to the providers mentioned in this piece for the best plan.

Whether UBI is the right car insurance solution for you, it’s always worth taking a minute to explore ways to lower your insurance premiums. Check out the resources available on Quote.com’s auto insurance page and be it with UBI or not, you’ll find even more ways of keeping money in your wallet.

Finding the right words are hard. Learning how to save on car insurance is easy at Quote.com

Enter your zip code below to view companies that have cheap insurance rates.

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Brad Larson

Licensed Insurance Agent

Brad Larson has been in the insurance industry for over 16 years. He specializes in helping clients navigate the claims process, with a particular emphasis on coverage analysis. He received his bachelor’s degree from the University of Utah in Political Science. He also holds an Associate in Claims (AIC) and Associate in General Insurance (AINS) designations, as well as a Utah Property and Casual...

Licensed Insurance Agent

Editorial Guidelines: We are a free online resource for anyone interested in learning more about insurance. Our goal is to be an objective, third-party resource for everything legal and insurance related. We update our site regularly, and all content is reviewed by experts.